New York Community Bank’s (NYCB) credit rating being downgraded to junk status by Moody’s Investors Service.

Protecting Your Finances: Understanding Bank Failures and How Gold and Silver Can Help

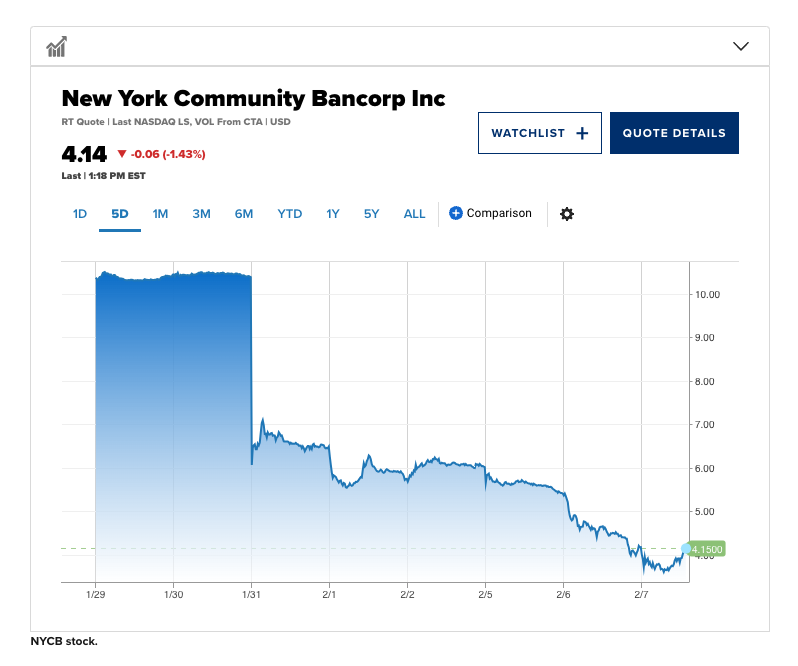

In recent headlines, the financial world was rocked by the news of New York Community Bank’s (NYCB) credit rating being downgraded to junk status by Moody’s Investors Service. This development sent shockwaves through the market, causing NYCB shares to plummet by as much as 13%. The downgrade came on the heels of a series of setbacks for the regional bank, including unexpected fourth-quarter losses and mounting challenges in its commercial real estate portfolio.

Understanding NYCB’s Crisis

NYCB’s troubles began when it reported a surprise fourth-quarter loss, coupled with increasing losses in its commercial real estate holdings. The bank’s decision to slash its dividend by a staggering 71% further rattled investors, leading to a significant decline in its market value. These developments underscored concerns about the bank’s profitability and raised questions about its ability to weather the storm in an increasingly challenging economic environment.

Management Shakeup

To address mounting concerns and stabilize operations, NYCB swiftly promoted its chairman, Alessandro DiNello, to the role of executive chairman. This move aimed to bolster leadership and reassure investors amidst the turbulence. DiNello, who previously served as CEO of Flagstar Bank, brings a wealth of experience to his new role and is tasked with collaborating closely with CEO Thomas Cangemi to improve the bank’s overall performance.

Moody’s Downgrade and Governance Challenges

Moody’s downgrade of NYCB’s credit ratings to junk status highlighted underlying financial, risk-management, and governance challenges facing the bank. Concerns were raised about turnover in key risk management positions and the need for stronger governance practices, particularly during a period of transition. The downgrade underscored the importance of robust control functions in mitigating risks and maintaining a bank’s credit strength.

Addressing Concerns

In response to Moody’s downgrade, NYCB emphasized its commitment to addressing governance issues and strengthening its risk management framework. The bank is actively searching for a new chief risk officer and chief audit executive to fill critical leadership roles. While interim managers are currently serving in these positions, NYCB acknowledges the need for permanent appointments to instill confidence in stakeholders and enhance oversight.

Protecting Deposits

Amidst the turmoil, NYCB sought to reassure depositors by providing unaudited financial information indicating that the majority of deposits were either insured or collateralized. This disclosure aimed to alleviate concerns about the safety of deposits and underscored the bank’s liquidity position. Despite the challenges, NYCB reported minimal deposit outflows from retail branches, signaling confidence among customers in the bank’s stability.

The Role of Gold and Silver in Financial Protection

In times of economic uncertainty and banking crises, investors often seek safe-haven assets to protect their wealth. Gold and silver have long been recognized as store of value assets that can provide a hedge against inflation, currency devaluation, and financial instability. Unlike fiat currencies, which are subject to government manipulation and central bank policies, precious metals offer a tangible and independent store of wealth.

Why Gold and Silver?

- Intrinsic Value: Gold and silver have inherent value derived from their scarcity, durability, and demand across various industries. Unlike paper assets, which can become worthless in the event of a financial collapse, precious metals retain their value over time.

- Diversification: Including gold and silver in a diversified investment portfolio can help mitigate risk and preserve wealth during periods of market turbulence. Precious metals often exhibit low correlation with traditional assets like stocks and bonds, making them an effective diversification tool.

- Liquidity: Gold and silver are highly liquid assets that can be easily bought, sold, and traded in global markets. This liquidity ensures that investors can convert their holdings into cash quickly and efficiently, providing financial flexibility during times of crisis.

- Historical Store of Value: Throughout history, gold and silver have served as reliable stores of value and mediums of exchange. Their enduring appeal as precious metals has stood the test of time, making them a trusted asset class for wealth preservation.

Protecting Against Fraud and Bank Failures

In addition to their role as safe-haven assets, gold and silver can also serve as a safeguard against fraud and bank failures. Unlike traditional bank deposits, which are subject to counterparty risk and potential loss in the event of a bank failure, physical gold and silver are tangible assets that are not dependent on the solvency of financial institutions.

Conclusion

In conclusion, recent headlines highlighting NYCB’s credit rating downgrade underscore the importance of understanding the risks inherent in the banking system. While banks play a crucial role in the economy, they are not immune to financial challenges and regulatory scrutiny. By diversifying their portfolios and including assets like gold and silver, investors can enhance their financial resilience and protect against the uncertainties of the banking system.

credit rating being downgraded to junk status by Moody’s Investors Service){kind=link}